by Allison Boden, on Aug 24, 2021 9:16:54 AM

In today’s labor market, it can be extremely difficult to find quality labor. The effects of COVID-19 and responses to the pandemic continue to drive wages up. Distribution employers will need to stay ahead of these trends to control costs in the coming years and budget accordingly. Site Selection Group, a leading location advisory, real estate and economic incentive services firm, looked at wage escalation in the distribution center industry to understand national trends.

Distribution center activity heavily gravitates to populated markets

Due to a variety of factors including access to consumers, availability of workers and robust transportation networks, most distribution center activity is focused on large metro areas. For this reason, SSG focused on metro areas with a population of more than 500,000 when researching wage inflation and how it correlates to occupation concentration. There are 111 metro areas in the United States that fall into this category.

According to the Emsi, the average annual wage inflation for distribution center occupations in the United States over the past five years was 3.5%. Although this number seems low given Site Selection Group’s recent project experience, it is the best relative indicator from one metro area to another over time. Conventional thought would be that wage inflation is higher in markets that have high distribution center activity as the competition for employment is greater. To evaluate activity, Site Selection Group looked at a basic metric of a location quotient which compares a metro area’s concentration of employment to that of the national average. A location quotient of 1 means that a metro is has the same concentration of that occupation compared to the national average.

High wage escalation in the western U.S. and other major markets

The following table shows the 10 metro areas with the highest five-year average wage escalation. There is some geographic diversity among these communities, but four of the top 10 are located in California, and the remainder tend to be very active markets for distribution activity.

| Metro Area | State | Average Wage Escalation | Concentration (1= National Average) |

| Tucson | AZ | 5.30% | 0.77 |

| Los Angeles-Long Beach-Anaheim | CA | 4.90% | 0.95 |

| San Jose-Sunnyvale-Santa Clara | CA | 4.90% | 0.52 |

| Dallas-Fort Worth-Arlington | TX | 4.90% | 1.13 |

| San Diego-Chula Vista-Carlsbad | CA | 4.90% | 0.74 |

| Chicago-Naperville-Elgin | IL-IN-WI | 4.80% | 1.22 |

| Oxnard-Thousand Oaks-Ventura | CA | 4.70% | 0.81 |

| New York-Newark-Jersey City | NY-NJ-PA | 4.70% | 0.92 |

| Lancaster | PA | 4.60% | 1.48 |

| Columbus | OH | 4.60% | 1.27 |

Source: Emsi, Transportation and Material Moving Occupations

The following table shows the 10 metro areas with the lowest five-year average wage escalation. Again, there is large geographic diversity in the results, but SSG expects wages to continue to escalate due to changes in minimum wage laws and continued demand for workers with these skill sets.

| Metro Area | State | Average Wage Escalation | Concentration (1= National Average) |

| Columbia | SC | 1.80% | 1 |

| Richmond | VA | 1.90% | 1.02 |

| Las Vegas-Henderson-Paradise | NV | 2.00% | 1.04 |

| New Haven-Milford | CT | 2.10% | 0.95 |

| Scranton-Wilkes-Barre | PA | 2.10% | 1.63 |

| Stockton | CA | 2.10% | 2.15 |

| Harrisburg-Carlisle | PA | 2.10% | 1.54 |

| Kansas City | MO-KS | 2.10% | 1.06 |

| Fayetteville-Springdale-Rogers | AR | 2.20% | 1.36 |

| Tulsa | OK | 2.20% | 0.88 |

Finding areas with talent but modest wage escalation

In the battle to hire and retain a qualified workforce, distribution center operators need to balance finding markets with trained talent with those that have manageable workforce costs. The following table shows the 10 metro areas with the highest location quotient that have a historical average wage escalation below the average of 3.5%. This includes, for example, a traditional distribution center market in Memphis, active distribution markets in Pennsylvania, and a California market, Stockton.

| Metro Area | State | Average Wage Escalation | Concentration (1= National Average) |

| Stockton | CA | 2.10% | 2.15 |

| Memphis | TN-MS-AR | 3.20% | 1.89 |

| Scranton-Wilkes-Barre | PA | 2.10% | 1.63 |

| Allentown-Bethlehem-Easton | PA-NJ | 2.20% | 1.61 |

| Harrisburg-Carlisle | PA | 2.10% | 1.54 |

| Fayetteville-Springdale-Rogers | AR | 2.20% | 1.36 |

| Greensboro-High Point | NC | 3.10% | 1.35 |

| Nashville-Davidson-Murfreesboro-Franklin | TN | 3.20% | 1.2 |

| Cincinnati | OH-KY-IN | 3.00% | 1.19 |

| Charlotte-Concord-Gastonia | NC-SC | 2.50% | 1.18 |

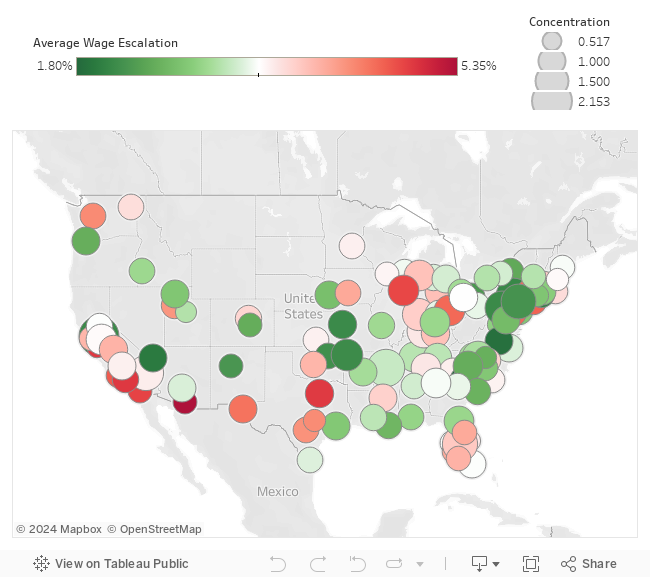

The following interactive map includes concentration and wage escalation data for all 111 metro areas with a population greater than 500,000. Hover over a point for more details.